✨ TAKEWAY

- Anthropic is reportedly targeting its first positive quarter, with revenue projected to double in Q2 2026. Its infrastructure costs are falling (71 → 56 cents per dollar of revenue)

- Going from red to green in under 6 months raises questions. Rather than revenue of $10.9 billion, we’re likely looking at $5.25 billion for Q2.

- Claude models remain unprofitable: zero gross margin from 20% usage for Pro and Max 5x, and 10% for Max 20x.

Is Anthropic in the Same Situation as OpenAI?

The article explaining just how deep in the shit OpenAI is paints a very bleak picture. With staggering infrastructure and R&D costs, impossible economies of scale, a loss of market share, and enormous debt, one might wonder whether Anthropic risks meeting the same fate.

And yet, the company is reportedly poised to potentially achieve its first positive quarter (Jin, 2026).

The news published in the Wall Street Journal reportedly announces that the company expects to double its revenue for Q2 2026. Although uncertain at this time, Anthropic’s trajectory stands out with growth higher than Zoom’s during the pandemic, and the company is benefiting greatly from the wave of popularity carrying it since the start of the year.

Green Signals

The Wall Street Journal indicates that Anthropic has seen a decrease in its infrastructure costs, dropping from 71 cents for every $1 of revenue in the first quarter to 56 cents per $1 of revenue in the second quarter. What enables such optimization is the use of GPUs developed by Google and Amazon, rather than Nvidia. The latter being much more expensive. Furthermore, the company benefits from a smaller user base, which limits spending on those who use it for free.

Anthropic can also count on additional revenue, as it sells its technology to cloud partners—something OpenAI cannot do (Jin, 2026).

Too Good to Be True?

Some are surprised by such an announcement. How can a company go from red to green in less than 6 months? Some hypotheses suggest that Anthropic is anticipating a certain amount of user demand as a form of prepayment, which inflates accounting revenue (Zitron, 2026).

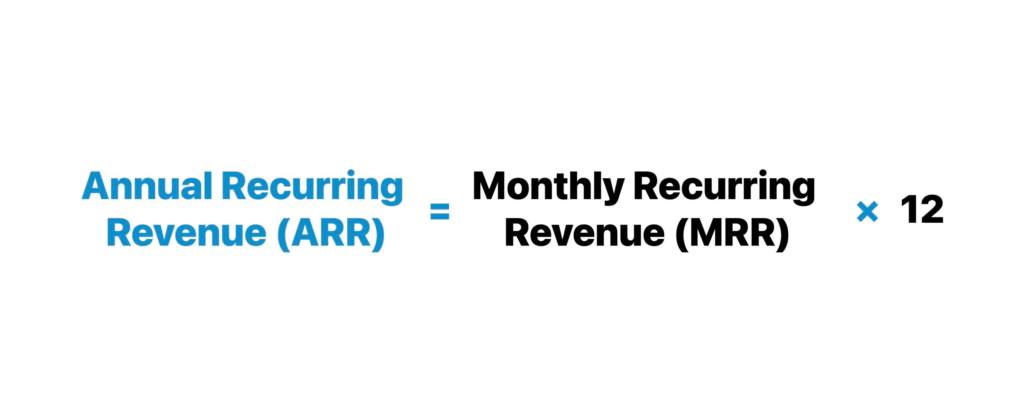

One of the biggest arguments is that this so-called projection of billions in profits for Q2 (compared to $4.8 billion for Q1) would be an ARR (annual recurring revenue), which represents a projection far from the revenue actually earned. Ed Zitron estimates that revenue for Q2 would amount to $5.25 billion.

Far from the $10.9 billion heard previously.

It is hard to buy into such potential revenue when all the company’s previous financial projections have proven to be inflated. Moreover, and as observed with OpenAI, AI companies often combine expansion with rising costs. So why not for Anthropic?

No Margin From 20% Usage

Claude models are far from profitable; the break-even point becomes nonexistent after just 20% usage for Claude Pro and Max 5x, and the Max 20x plan reaches zero gross margin at 10% usage (Gautam, 2026).

What Solutions Are Possible?

The solution everyone is talking about to attract investors would be for Anthropic to go public through an IPO (Initial Public Offering), in other words, the stock market. Still, greening a balance sheet with startup techniques like ARR and being truly profitable are two different things. As long as the cost per token exceeds what subscription users pay, the question of profitability will remain for Anthropic.

Sources :

Gautam, A. (2026, June 16). SemiAnalysis: ChatGPT Pro Costs OpenAI $14,000 at Full Use — The Agentic Subsidy Exposed. Abhs.In. https://abhs.in/blog/chatgpt-pro-200-costs-openai-14000-semianalysis-agentic-token-explosion-2026

Jin, B. (Mai, 2026). Mind-Blowing Growth Is About to Propel Anthropic Into Its First Profitable Quarter. The Wall Street Journal. www.wsj.com/tech/ai/mind-blowing-growth-is-about-to-propel-anthropic-into-its-first-profitable-quarter-7edbf2f4?

Zitron, E. (Mai, 2026). Anthropic’s “Profitability” Swindle. Ed Zitron’s Where’s Your Ed At. https://www.wheresyoured.at/anthropics-profitability-swindle/